Impermanent loss refers to the loss that liquidity providers (LPs) might experience when they supply assets to a DeFi liquidity pool, compared to simply holding those assets outside the pool. This phenomenon occurs due to the fluctuations in the prices of the tokens within the liquidity pool. To better understand impermanent loss, it’s essential to know the mechanics of automated market makers (AMMs) and how they function.

The Basics of Liquidity Pools and AMMs

In DeFi, liquidity pools are the backbone of decentralized exchanges (DEXs), where users trade cryptocurrencies without a traditional order book. Liquidity pools consist of pairs of tokens (e.g., ETH/USDT), and LPs provide these tokens to the pool to facilitate trading. In return for providing liquidity, LPs earn a portion of the trading fees generated from the pool.

AMMs use algorithms to determine the price of tokens in the pool based on their relative supply. The most common algorithm used is the constant product formula (x * y = k), where “x” and “y” represent the quantities of the two tokens, and “k” is a constant. As traders swap one token for another, the quantities change, but the product remains constant, which in turn affects the price.

What is Impermanent Loss?

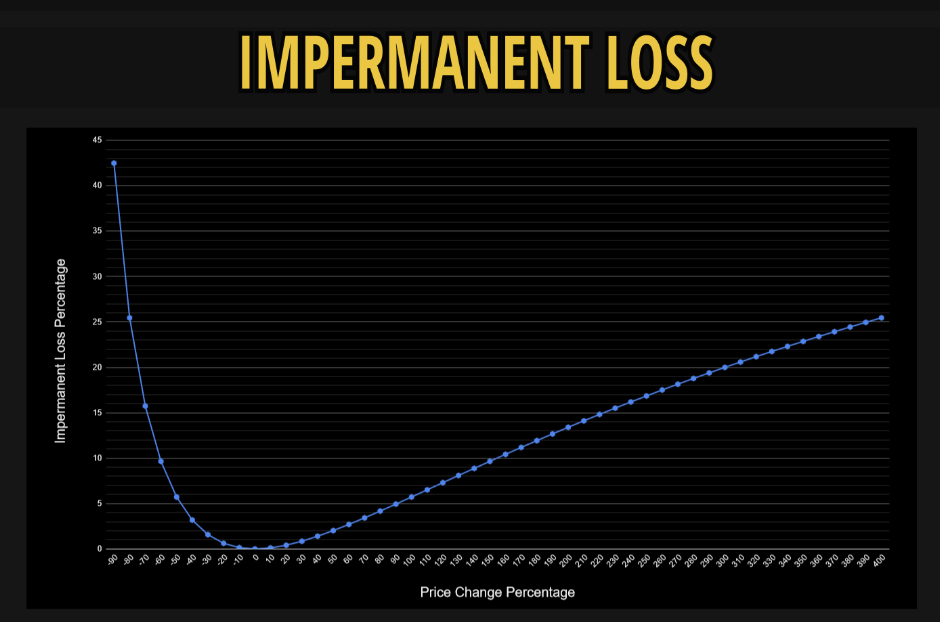

Impermanent loss is the reduction in value that occurs when the price of the tokens deposited in a liquidity pool changes compared to their price at the time of deposit. The divergence can either be an increase or decrease in one or both token prices relative to each other (Figure 1). This loss is termed “impermanent” because it is only realized if the LP withdraws their liquidity when there is a price disparity; if the prices return to their original state, the loss is theoretically nullified.

Figure 1: Impermanent Loss Curve on Constant Product Pool Example

Source: James Bachini

However, if the price deviation persists or widens over time, the LP stands to lose value compared to holding the tokens outside the pool.

Case Study: SUSHI-WETH Pool on SushiSwap During the SUSHI Price Collapse

In September 2020, SushiSwap faced a crisis when the anonymous founder “Chef Nomi” sold a significant portion of the SUSHI tokens, leading to a collapse in SUSHI’s price. The SUSHI-WETH pool experienced a severe impermanent loss due to the rapid depreciation of the SUSHI token.

As the price of SUSHI plummeted by over 80% within a short period, LPs in the SUSHI-WETH pool found themselves holding increasingly larger amounts of SUSHI (the depreciating asset) while losing WETH. The AMM rebalanced the pool in response to the price drop which resulted in LPs holding a larger proportion of the less valuable asset.

The LPs who provided liquidity during the crash saw impermanent losses exceeding 50%. Additionally, the negative sentiment around SushiSwap led to a liquidity exodus and further deepened losses for those who remained in the pool. This event underscored the risks associated with providing liquidity to pools which consist of highly speculative or newly launched tokens.

Calculating Impermanent Loss

The calculation of impermanent loss depends on the degree of price divergence between the two tokens. If the price of one token increases relative to the other, the liquidity pool automatically rebalances the quantities of each token to maintain the constant product formula.

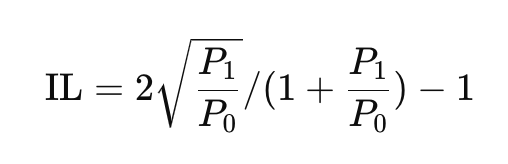

The formula for calculating impermanent loss (IL) in constant product pool is:

Where:

- P0 is the initial price ratio between the two tokens.

- P1 is the new price ratio after divergence.

To illustrate, consider an ETH/USDT liquidity pool on a DEX. Suppose an LP deposits 1 ETH (priced at $2,000) and an equivalent amount of USDT ($2,000), with a total initial value of $4,000. If the price of ETH rises by 50% to $3,000, the AMM will adjust the asset ratio in the pool to maintain the constant product formula by reducing the amount of ETH and increasing the amount of USDT in the pool. If the LP withdraws their liquidity at this new price, they will end up with less ETH and more USDT than initially deposited. If the LP had held 1 ETH and $2,000 USDT outside the pool, the new total value would be $5000. Inside the pool, due to the impermanent loss, the total value would be around 5.72% less, or approximately $4,715. However, it will still exceed the original $4,000.

There are impermanent loss calculators which are special tools designed to estimate the potential losses a user might face when providing liquidity to a particular pool. These calculators consider various factors, including the initial prices of the assets, the composition of the pool, and changes in prices over time.

Here are examples of impermanent loss calculators:

- STON.fi’s Impermanent Loss Calculator

- CoinGecko’s Impermanent Loss Calculator

The Role of Fees in Offsetting Impermanent Loss

Fees play a crucial role in offsetting impermanent loss. When a trader swaps tokens in a liquidity pool, they pay a fee (usually a small percentage of the trade value), which is distributed among LPs. In high-volume pools or pools with high fees, the income generated from these fees can outweigh the losses caused by price divergence.

For example, if a liquidity pool has a 0.3% fee on trades and experiences a high volume of trading, the accumulated fees might be sufficient to compensate for substantial impermanent loss and result in a net gain for the LP. Hence, when considering which pools to provide liquidity to, LPs should assess the potential for impermanent loss and also the expected fee income.

Some DEXs, such as STON.fi and Uniswap v3, employ dynamic fee structures that adjust fees based on market volatility and trading volume. During periods of high volatility, fees increase to compensate LPs for the elevated risk of impermanent loss, but during stable periods, fees decrease to encourage trading activity. This dynamic approach offers higher compensation for LPs during turbulent market conditions and reduces impermanent loss due to higher fee revenue.

Factors Affecting Impermanent Loss

Several factors influence the extent of impermanent loss experienced by an LP:

- Price Volatility: Higher volatility in the prices of the tokens within a pool leads to greater impermanent loss. Stablecoin pairs generally exhibit lower impermanent loss compared to more volatile assets.

- Liquidity Position Duration: The longer an LP remains in a pool, the higher the probability of experiencing price divergence and, hence, impermanent loss. However, this can be offset by the fees earned over time.

- Fee Structure: Fees earned from trades in the pool can mitigate or even outweigh impermanent loss. High-volume pools or those with lucrative fee structures can provide enough earnings to compensate for potential losses.

- Type of Pool: AMMs employ various algorithms for liquidity and pricing management. For example, constant product formula can lead to significant impermanent loss in volatile markets. Pools with customizable weights, such as Weighted Pool, mean that the pool doesn’t have to hold a 50/50 ratio of assets. This can mitigate the effects of impermanent loss to some extent if properly set. Stablecoin pools such as StableSwap and Wstableswap can reduce the impermanent loss even further because they consist of stable assets with minimal price divergence.

The Psychology of Impermanent Loss

While the technical mechanisms of impermanent loss are well understood, the psychological factors influencing how liquidity providers perceive and react to impermanent loss are often overlooked. In behavioral economics, phenomena like loss aversion and cognitive biases play a significant role in decision-making.

Here are several behavioral patterns in response to experiencing impermanent loss:

Overreaction to Short-Term Volatility: Many LPs might react emotionally to short-term price fluctuations and are frightened by impermanent loss. Therefore, they will withdraw their liquidity hastily and lock in losses that could have been mitigated if they had waited for price recovery. This behavior is akin to panic selling during a market downturn, driven by fear rather than rational analysis.

Endowment Effect in DeFi: The endowment effect, where individuals value an asset more simply because they own it, can lead LPs to overestimate the potential value of their held tokens outside the pool. As a result, they might avoid participating in pools or withdraw early, fearing impermanent loss, even when the actual risk-adjusted returns could be higher if they remained in the pool.

Anchoring Bias and Decision Paralysis: LPs often anchor their expectations to specific price points or previous returns, which can lead to decision paralysis. For example, if an LP enters a pool when token prices are at a certain level, they may be overly focused on those initial prices, hesitating to act in response to new market conditions.

Strategies to Mitigate Impermanent Loss

Although impermanent loss is an inherent risk for LPs in DeFi, several strategies can help mitigate its impact:

- Selecting Low-Volatility Pairs: Providing liquidity for pairs with low volatility (such as stablecoin-stablecoin pairs) reduces the likelihood of significant price divergence and minimizes impermanent loss.

- Diversification Across Multiple Pools: Spreading liquidity across multiple pools can diversify the risk. By choosing pools with different risk profiles, LPs can balance potential losses from one pool with gains from another.

- Pools with Higher Trading Fees: Participating in pools with higher trading volumes and fees can help compensate for impermanent loss. The fees earned from trading activity can offset the loss, especially in high-volume pools.

- Active Liquidity Management: Active management of liquidity through market conditions monitoring and liquidity positions adjustment based on price movements or volatility trends can reduce exposure to impermanent loss. This strategy requires constant vigilance and a good understanding of market dynamics.

- Providing Liquidity in Concentrated Ranges: Some AMMs, such as Uniswap v3, allow LPs to provide liquidity within specific price ranges and hence concentrate liquidity around the current price. This can increase capital efficiency and reduce exposure to impermanent loss in case the price remains within the selected range.

- Mitigate Psychological Biases: To counteract these biases, DEXs can offer tools such as psychological nudges, clear educational content, and simulators that show potential scenarios of impermanent loss and recovery. Additionally, transparency about potential risks and rewards, along with dynamically updated analytics dashboards, can help LPs make decisions based on data rather than emotion.

Impermanent Loss vs. Permanent Loss

It is important to differentiate impermanent loss from permanent loss. Impermanent loss refers to the potential loss of value compared to simply holding the assets due to price divergence. It becomes “permanent” only when the liquidity is withdrawn at a time when prices have diverged unfavorably. If the prices return to their original state, the impermanent loss may be completely nullified and thus truly “impermanent.”

Permanent loss, on the other hand, occurs if an LP exits the liquidity pool when prices are unfavorable and locks in the loss. Therefore, the timing of withdrawal from a liquidity pool is one of the critical factors for LPs to consider.

Case Study: UST-LUNA Pool on TerraSwap During the Terra Collapse

In May 2022, the Terra ecosystem collapsed when its algorithmic stablecoin UST lost its peg to the US dollar, triggering a death spiral for both UST and its paired token LUNA. The UST-LUNA liquidity pool on TerraSwap saw massive losses as LUNA’s value plummeted from over $80 to less than a cent.

As UST depegged and its value fell sharply, the AMM rebalanced the pool by increasing the amount of LUNA held and reducing the amount of UST. With LUNA’s rapid decline in value, LPs ended up with a massive amount of nearly worthless LUNA tokens, while losing UST, which was already suffering from de-pegging.

LPs faced near-total losses, with many losing over 99% of their holdings in the pool. This event emphasized the risks associated with providing liquidity to pools containing algorithmic stablecoins and poorly designed tokenomics that can lead to cascading failures.

Conclusion

Impermanent loss represents a significant risk for liquidity providers in the DeFi space, especially when dealing with volatile or poorly designed assets. Understanding how impermanent loss works and the various strategies to manage it allows LPs to make informed decisions and balances the risks and rewards of providing liquidity in the DeFi ecosystem.